10 June 2014

Kuala Lumpur International Airport Terminal 2 (klia2) uniquely aims to be a model of connectivity for all low-cost carriers in the region.

Kuala Lumpur International Airport’s new low cost terminal (LCT) – klia2 – which opened at the beginning of May-2014 after several delays and an estimated MYD2.6 billion (USD803.2 million) budget overrun to around USD1.2 billion, is paradoxically attempting to be a hit with low-cost carriers as a connection / transfer point.

'Paradoxically’ because ‘low cost’ and ‘passenger transfers’ do not usually sit comfortably with each other. We have already witnessed the birth and growth of a new trend generated by the LCCs – ‘self connection’ – but a reported near 50% of passengers on long-haul LCC AirAsia X expected to take connections though klia2, while the short/medium-haul AirAsia moves in the same direction, is something else and would be quite a breakthrough for this transport medium.

It is instructive to take an overview of how klia2 came to be built at all, and how the original budget terminal at Kuala Lumpur quickly became too small partially as a result of the incredible growth of AirAsia.

Kuala Lumpur vied with Singapore for supremacy in a fledgling low-cost aviation environment

Essentially, the first budget terminal at Kuala Lumpur International Airport and the eponymous (and now abandoned) ‘Budget Terminal’ at Singapore Changi Airport were built to compete with each other for predominance in the then relatively fledgling low-cost air transport environment in Southeast Asia.

Indeed the two terminals opened within a month of each other in Mar-2006.

For some time the two remained the primary examples of this sort of structure in Asia. Bangkok did not respond in a like manner and became embroiled in endless discussions over what to do with its Don Mueang Airport when Suvarnabhumi Airport opened, again in 2006.

Only fairly recently (2012) has Don Mueang been given the chance to prove its mettle as a budget airport facility, which is what it probably should have been for the last eight years.

The host airport in Malaysia, Kuala Lumpur International Airport or KLIA, opened in 1998 at a cost of USD3.1 billion and is situated in Malaysia’s ‘Silicon Valley’, but 60km south of the capital. The alternative, Subang Airport, was much closer (20km) and had been considered for conversion into a low-cost airport previously.

After KLIA was constructed it was then earmarked for decommissioning and conversion into a maintenance, airfreight, warehousing and distribution facility (as was Don Mueang airport in Bangkok).

However, a series of system failures immediately after KLIA’s opening, together with surface transport hold-ups, meant that some domestic airline operations were temporarily retained at Subang, and Malaysia Airlines (MAS) relocated some domestic services back there following a drop-off in traffic.

Amongst the carriers staying at Subang was AirAsia, which then, as now, was led by the mercurial Tony Fernandes, a character in the colourful man-on-a-mission mould of Virgin Atlantic’s Branson, Ryanair’s O’Leary and easyJet’s Hali-Ioannou.

During 2004, the year in which AirAsia held a successful IPO, the first for an Asian LCC, the government ordered the carrier to move to KLIA.

AirAsia’s Tony Fernandes was not keen to move to KLIA

But AirAsia, having just placed an order for 100 A320s, a whole new experience for an Asian LCC at the time, did not want to move to KLIA, which was considered inappropriate to the airline’s operating model. Mr Fernandes lobbied the government to keep both facilities open, quoting examples as disparate as Rome and Rio de Janeiro where two airports cater to different market sectors.

His attitude was encapsulated in the statement: “Give us Subang and we will give the Singaporeans a run for their money. Why not improve what we already have?” Subang would cost “only” MYR25 million to refurbish, as it was already an international standard airport while “KLIA is as packed as the Don Mueang airport in Bangkok and Heathrow in London”.

That was perhaps an exaggeration at the time; KLIA was designed to handle 60 million passengers by 2020 and it sprawls over 4,000 acres, one of the largest airport areas in the world.

The lower cost base at Subang, especially the reduced taxiing time at peak periods and consequentially reduced fuel burn, along with the airport’s proximity to the city, was critical to Mr Fernandes. He estimated the excess costs at KLIA to be of the order of 20%-30%. He also did not want to go head to head with MAS, a feeling that was reciprocated.

Moreover, it was going to cost his passengers an extra MYR35 one way to use the train to and from KLIA. KLIA management tried to be co-operative; to show that it was equally keen that the airport should work as a base for LCCs.

Landing and parking charges at Malaysian airports were broadly similar, the differentiation being with passenger charges. But Mr Fernandes still felt that profitability could be better achieved at Subang.

In Jun-2004, the Malaysian Ministry of Transport intimated it would consider designating Subang as a budget, point-to-point airlines base and commenced a study to investigate the value of that option versus building a low-cost terminal at KLIA.

By now the Ministry’s wider strategy was to make the country a “low-fare hub” for the region, to build on the strength and reputation of AirAsia. Naturally, MAS did not see things the same way and declared itself against any low-cost development at Subang.

As time progressed the Transport Ministry started to favour the plan to build a separate terminal for budget airlines at KLIA instead of reconstituting Subang Airport, on the basis that KLIA seemed a more logical choice to handle international flights of any variety. Moreover, a large sum had already been spent building KLIA.

In the end the Malaysian Government’s Cabinet unsurprisingly favoured KLIA over Subang.

It was decided that the low-cost terminal’s structure would be simple and basic, for example it would not include aerobridges, travelators or escalators, and it would be built quickly, the work commencing in Apr-2005.

The race was on to complete it before Singapore’s was finished to benefit from the prestige of being the ‘first’ in the region.

The projected cost was MYR50-100 million for a 35,000sqm edifice with 72 check-in counters. It would cater for up to 40 aircraft initially, offering a 20-minute turnaround and have an annual capacity of 10-12 million passengers with potential expansion capability to 50 million. The existing apron could accommodate 23 aircraft simultaneously, and could be extended to accommodate another 48 aircraft.

Food & beverage, retail and duty free facilities were provided, together with a foreign exchange counter, pay phones, auto teller machines, hotel reservation, car rental, taxi service and a prayer room.

Poor location of KLIA’s original low-cost terminal meant a very long road journey for some passengers

One very significant drawback right from the start though, was that it was located on the opposite side of the apron from the main terminal building, which meant a road journey of up to 20km for passengers switching between terminals or if they accidentally went to the wrong terminal. In contrast, Singapore’s LCT was a short drive from the main terminals. The government approved a rail link between the main terminal and LCT to tackle the problem.

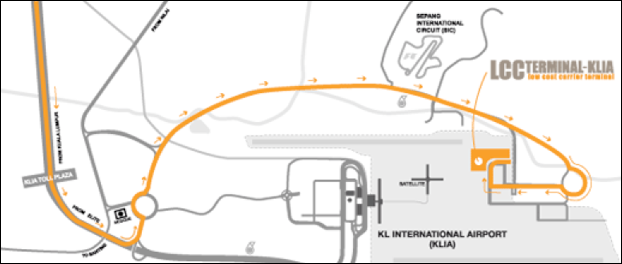

KLIA Locator Map: showing original LCT and Sepang F1 motor racing circuit

As a consequence of the construction, 2–3 million passengers per annum would be shifted away from KLIA’s existing congested LCC area until a new satellite was built there.

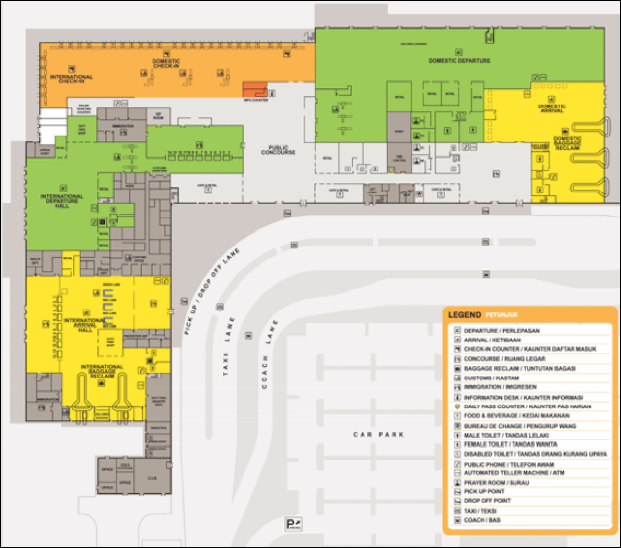

Overview of original LCT at Kuala Lumpur International Airport

AirAsia gave up the fight to stay at Subang

It was at this stage that AirAsia gave up the fight to remain at Subang, a press statement issued at the time from Tony Fernandes stating: “We will refocus and re-energise ourselves to focus on making the low cost terminal in KLIA into an efficient design for AirAsia’s low cost model, and make it into the centre for low cost travel in Asia despite stiff competition from Singapore.

"We will work closely with MAHB (Malaysia Airports Holding Berhad, the operator) to develop our country’s first dedicated low cost terminal that will serve to meet the needs and wants of a low cost airline. We are pleased that Malaysia Airports have delivered a blue print of KLIA that will almost mimic Subang in KLIA, even down to the low cost transport to the terminal.”

The final cost of the original LCT came to MYR108 million (about USD25 million), similar to the cost at Singapore and a price which is minuscule in comparison with the subsequent development of klia2.

Relatively few airlines chose to use the KLIA LCT, but more than at Singapore

There were different ways of assessing the LCT’s success. Apart from AirAsia, and as big as that airline is, there were few other users of the LCT terminal; mainly subsidiaries Thai AirAsia and Indonesia AirAsia, long-haul affiliate, AirAsia X, plus Cebu Pacific of the Philippines. Australia’s Jetstar commenced a three times weekly service in 2007, but it operated from the main terminal, reflecting Jetstar’s wish to access long-haul connecting traffic in that terminal (and in contrast with what is happening now).

Despite the relative paucity of airlines and because AirAsia became so big the terminal began to approach its capacity within two years. In 2007, passenger volume at KLIA reached 26 million, including seven million utilising the LCT.

MAHB approved expansion of the terminal and preparations were made to accommodate the use of bigger aircraft by AirAsia X for its operations subsequent to its operational start-up in Nov-2007.

The expansion was intended to take it up to 15 million ppa capacity from 10 million and would include a new food court. That expansion was completed in May-2009, extending the LCT to 64,067sqm, double its previous size.

It was about this time that MAHB first considered it might have to look for a new site altogether if the LCT reached the expanded maximum capacity. Already the budget terminal was outpacing Singapore Changi’s with three times as many passengers. Changi’s LCT was struggling to attract LCTs at all, some of which opted to use the main terminals, though it performed better at generating non-aeronautical revenues.

Alternative Labu LCT project influenced MAHB’s views on a bigger LCT at Kuala Lumpur

There was a domestic political factor behind MAHB’s decision as well. In 2008 a Malaysian-based multinational conglomerate, Sime Darby, together with AirAsia, concocted a proposal to construct a USD500 million low-cost airport in Labu, to be known as KLIAEast@Labu, with capacity for 25 million ppa, at that time at least 10 million ppa greater than the capacity at the original Kuala Lumpur LCT.

Moreover, it would be 8km closer to the capital. The proposed financial package was a private finance initiative.

Location of proposed Labu airport (denoted with red A)

Initially the government approved the project but later (end Jan-2009) changed its mind following the intervention of IATA (which argued in favour of further development of the KLIA ‘hub’ and against the traffic management implications of two neighbouring airports); also from Malaysia’s Khazanah Nasional Berhad, which holds a majority stake in MAHB. Khazanah Nasional stated it preferred to stick with the National Airport Master Plan as a lot of resources had already gone into it.

Despite the fact the government was supportive of the venture, as it would have boosted the country’s building industry that had been hit by recessions in many Asian countries, the project was later cancelled.

The original Kuala Lumpur LCT was intended to be an expandable terminal and indeed that happened, but if growth was going to reach previously unanticipated levels it was appropriate to be considering another new terminal, and one that had greater proximity to the central terminal and associated buildings.

By now MAHB forecast passenger traffic at the LCT would grow by 30% in 2009, reaching 300 aircraft movements per day, as LCCs launched new destinations and increased service frequencies, and believed the existing terminal would hit full capacity in 2011 with the majority of this growth coming from international traffic, forecasting slower than normal increases in domestic traffic.

A further LCT terminal became a reality and was earmarked early on to be a regional ‘hub’ for budget travellers

Early negotiations commenced for a permanent LCT for up to 30 million ppa, expandable to 45 million ppa, and MAHB quickly became committed to it. The terminal would boost overall capacity by 60% to 50 million ppa and the intention was that it would turn Kuala Lumpur into a major regional hub for budget travellers to combat KLIA’s inability to shift full service and hub/network traffic away from Singapore and Bangkok. It would be situated adjacent to the main terminal and be ready by 2010, later 3Q2011, and the earliest cost quoted was USD573.7 million.

The original LCT would be transformed into a cargo-handling terminal once the planned new LCT was completed.

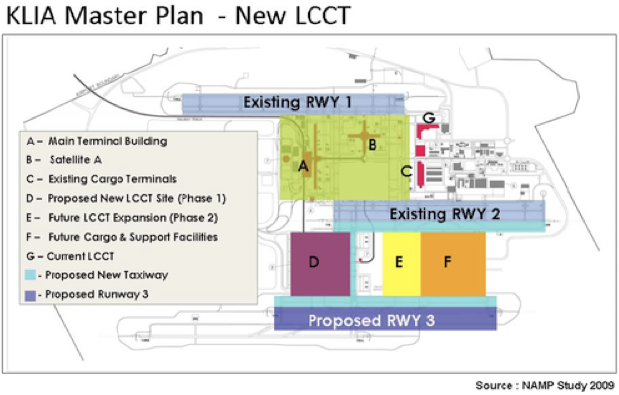

The new 150,000 sqm LCT would be located in Sepang, 1.5km from KLIA’s main terminal building. The main building and the new LCT would be linked by an Express Rail Link (ERL) connection. Early features of the new terminal included 6,000 car parking spaces, a transport hub both for buses and taxis and 70 aircraft parking apron bays. Furthermore, a third 4km runway would be built at KLIA to cater for the new terminal, as well as a parallel taxiway for Runway 2 and 3 to allow quick turnarounds.

Kuala Lumpur International Airport (KLIA) new LCCT master plan map: 2009

Thereon in, the construction of the new terminal was beset by cost and timeframe issues. The terminal’s completion and opening was successively rescheduled to 01-May-2013 and 28-Jun-2013 respectively, and the cost rapidly more than doubled to USD1.3 billion; the final price amounting to a budget overrun of around USD800 million.

The opening date was further put back by a month, then to 4Q2013 and eventually to 02-May-2014, the final delay and the sixth published completion date. The reason given was “insufficient resources.”

During this period and following re-evaluation of passenger traffic projections and LCC sector developments the terminal design was expanded to increase floor space from 150,000sqm to 250,000sqm (adding a third storey), increase the number of arrival and departure gates from 55 to 68, improve baggage handling systems and add a premium lounge at the request of AirAsia.

AirAsia also influenced the airport's decision to extend and widen its runway to accommodate larger aircraft. These additions contributed to the cost of the facility doubling in price and MAHB determined to raise at least MYR1 billion (USD306 million) through Islamic bonds to finance its completion.

At that stage it was determined that klia2 would no longer be a dedicated low-cost terminal.

KLIA's third runway was completed specifically to support klia2

In Oct-2013 KLIA completed construction of its third runway, specifically as a part of the klia2 project, followed by the supporting infrastructure two months later. The runway measures 3960m by 60m and is capable of handling any current aircraft fully loaded. Malaysia is the first country in the region to have a third runway for its flagship airport.

Despite further slippages in the terminal construction schedule it opened with ICAO and FAA approval on 02-May-2014 following a safety evaluation that found only small cracks on the apron parking and taxiway. The original LCT closed on 09-May-2014.

There were some subsequent infrastructure issues and at the time of writing they have not been eradicated. The most significant is the appearance of depression pits – or ‘sinkholes’ – at klia2’s airfield. IPC (Ikram Premier Consulting), which previously had determined that the new terminal met ICAO and FAA standards, has been reappointed along with ICAO to investigate the event.

Kuala Lumpur International Airport's klia2

The terminal is accessible via six highways and has its own dedicated spur access road.

klia2 access roads

The final klia2 specification is as follows:

- Built-up area of 257,000 sqm with 68 departure gates, eight remote stands, 80 aerobridges;

- Retail space of 35,000 sqm to accommodate a total of 160 retail and food and beverage outlets throughout the main terminal, with an additional 170 retail and dining outlets at the adjoining Gateway@klia2 complex;

- Four check-in islands with a total of 128 Common User Passenger Processing System (CUPPS) check-in counters. There are also 55 self-service check-in kiosks. There are 14 Royal Malaysian Customs checkpoints at klia2, with seven located each at the arrivals and departures halls respectively. The terminal has an airport sky bridge, the first such structure in Asia and the third in the world.

- A green building with Leadership in Energy & Environmental Design (LEED) certified;

- A dedicated 4 km runway (Runway 3) with a 2.2 km separation distance from Runway 2 at KLIA allows simultaneous aircraft take-off and landing operations at KLIA, the first of its kind in the region;

- Gateway@klia2 is an integrated airport-within-a-mall complex that hosts an eight storey car park that directly adjoins klia2. There are 6,490 covered parking bays with 5,690 car bays and 800 motorcycle bays at Blocks A and B, and another 5,500 lots at car park D.

- klia2 is connected with the Express Rail Link (ERL) service (also known as KLIA Ekspres) at the adjoining Gateway@klia2 complex, and the ERL/KLIA Ekspres service offers connectivity to the heart of Kuala Lumpur, terminating at the KL Sentral station in the city. The Gateway@klia2 complex also accommodates all public transport services serving klia2, including buses, taxis and car rentals;

- Residential facilities. Sama-Sama Express Hotel klia2 is an airside transit hotel at Level 3, satellite building. Sama-Sama Express klia2 has 70 rooms, and hotel guests do not need to clear Malaysian customs and immigration if they are on a layover between flights. Adjacent to the terminal is the Tune Hotel at klia2, and the hotel is directly linked by a covered walkway. The first capsule transit hotel in Asia named as the Container Hotel will also be opening at klia2.

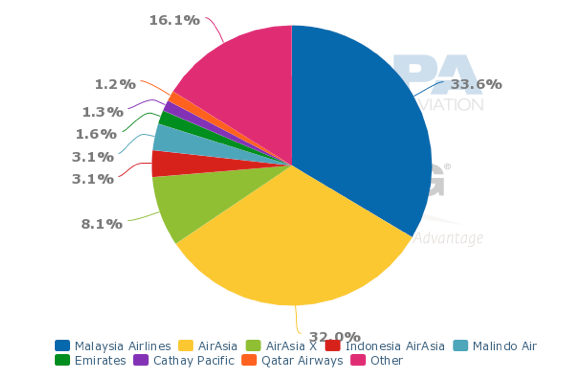

klia2 is undeniably a project has spiralled to deliver ultimately the largest facility for low-cost airlines (even if it can host others) in the world and one that can cater for more than twice the number currently handled by London Stansted airport. At the time of writing all the airlines using it are LCCs and they are AirAsia (Domestic and International); AirAsia X; AirAsia Zest; Indonesia AirAsia; Thai AirAsia; Lion Air; Cebu Pacific; Tigerair; Malindo Air.

The six airlines that were operating at the original LCT in 2009 when the decision to build klia2 was taken are italicised above. (Tigerair then as Tiger Airways).

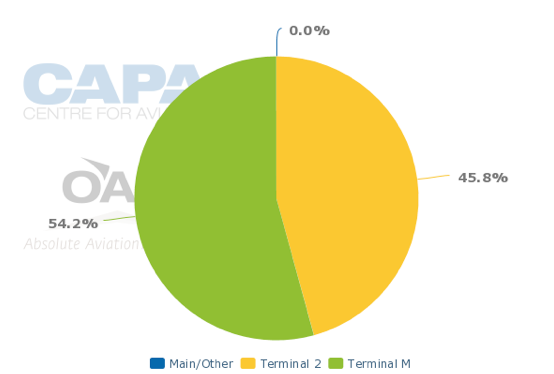

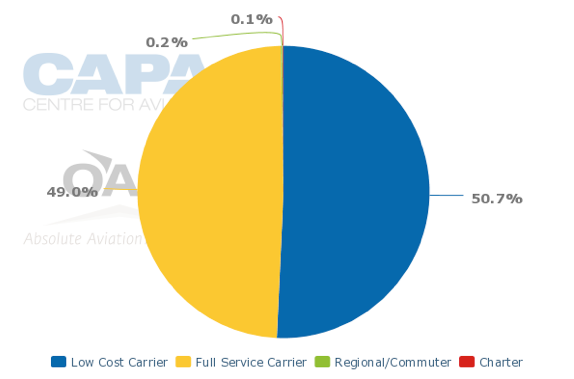

In terms of overall seat capacity at KLIA in May-2014 (see third chart below), AirAsia and Malaysia Airlines (MAS) are running virtually neck and neck with about one third of that capacity each. MAS continues to use the main terminal.

Kuala Lumpur International Airport terminal share (seats) by total system: 26-May to 01Jun-2014

Note. In this chart:

Terminal M = the original non-LCC terminal, being both the main and the satellite as it refers to the check-in/arrival area

Terminal 2 = the designation for the new LCCT being klia2

Main/other – (0%) reflects the cargo only services that require no passenger check-in

Kuala Lumpur International Airport capacity seats share by carrier type: 26-May to 01-Jun-2014

There was mounting criticism during the latter part of the construction project for klia2, directed both at its cost and at its scale. There is no other contemporary structure in the world that is directly comparable, certainly not in Bangkok, Hong Kong or Manila, and it was conceived and built during the period when a misfiring budget terminal at Singapore was identified for closure.

It is interesting to note the way in which AirAsia’s Tony Fernandes, who not so long ago was totally opposed even to moving to KLIA from Subang, has embraced the new terminal and its comparatively luxurious outfitting. Indeed, Mr Fernandes lobbied hard for a premium lounge and influenced the airport's decision to extend and widen its runway to accommodate larger aircraft.

An internal view of klia2’s premium lounge.

In an online briefing he is reported to have said that MAHB complied with almost everything requested by AirAsia for it to operate from klia2 – except for a spa and a museum. Furthermore, he acknowledged that the LCC is set to be “the biggest gainer” by operating from the new airport and is expected to contribute about 80% of the new terminal’s traffic.

Perhaps this is because the visionary in Mr Fernandes acknowledges the growing drift worldwide of LCCs towards hybridity, by which they more consistently respond to the needs of business travellers. Or perhaps because he has been able to envisage the potential for long-haul to long-haul and long-haul to short-haul connectivity within the LCC domain, a pattern that remains at a nascent level globally just yet. He will be aware thatAustralia’s Jetstar had one-stop long-haul expansion plans to Europe that would require the establishment of an Asian hub.

AirAsia X is once again talking about recommencing European long-haul budget flights once it has the aircraft to operate them profitably and is happy to embrace the concept of self-connection at the airports it uses. (When it operated to London Stansted airport several years ago it was reported that up to 30% of its passengers then took on onward flight on another airline on a separate ticket, if not always on the same day). Further afield, Norwegian Air Shuttle has grand plans for long-haul low-cost from London Gatwick, Madrid and other airports and is ruffling feathers in the United States, while Ryanair’s Michael O’Leary continues to drop hints that his own intentions for long-haul operations have not diminished.

There are certainly factors in place at klia2 to aid the concept of such connectivity.

Although all operators momentarily are LCCs there is nothing to stop any carrier operating there, such as a full service unaligned carrier to cooperate with one or more local LCCs and the physical size of the building, which is bigger than the main terminal by some margin, would further facilitate such activity.

In a recent interview with CAPA, the general manager for special projects at MAHB, Mr K Veelayudan Nair, pointed out that while the former KLIA LCT was built as a dedicated temporary terminal for low-cost operations it was only a temporary solution as the AirAsia operations began to cause congestion at the main terminal and was hindering its growth. The KLIA LCT had many weaknesses to be overcome with the new klia2.

Thus klia2 was primarily built for the use of low-cost carriers but also is suitable and open for other airlines, not exclusively for LCCs. This was decided as early as at the time of the ground breaking ceremony.

'There is no such thing as a low cost terminal meant only for low cost carriers'

In fact, according to Mr Nair, MAHB believes that there is no such thing as a low-cost terminal meant only for low-cost carriers. In fact, the question to ask is "what is the definition of a low cost terminal?"

He enlarges on this position by saying that an airport has to meet safety and security requirements and this cannot be compromised. How can these requirements be less for the terminal that caters for low-cost airlines? If at all, the only compromise could be on the level of comfort that is accorded to passengers. How low could an operator go on these levels?

Could the terminal go without air conditioning in a hot-humid environment such as in Malaysia? Can the operator get away with providing no seating? As an airport operator MAHB would not want its passengers to sit on the floor.

Airlines prefer aerobridges in the wet Malaysian climate

He adds: “We can dispense with aerobridges but it has other implications such as security and safety issues due to movements on the airside that need proper control. For short haul flights compulsory aerobridge usage can cause some extra time for turnaround which may prevent maximum utilisation of aircraft.

"In fact we realised that airlines preferred aerobridges in a wet environment like Malaysia. In the past we have seen many flights have continuously been delayed due to rain! The consequential effect on schedules even due to a 15 minute morning rain shower can be very serious. Ultimately, we have given options to airlines to use or not to use aerobridges”.

klia2 is indicative of the direction ‘low cost terminals’ will take in the future

So apart from its size, and cost, klia2 seems to be indicative of the direction ‘low cost terminals’ are going to take in the future: designed primarily for LCC use but not exclusively so, with comfort features not previously considered essential in this type of edifice, and mindful of the changing mores of the ‘low cost’ business globally as it seeks to attract more business travellers and even changes its attitude towards aerobridges and their propensity to slow what was hitherto considered the sacrosanct business feature of the rapid turnaround.

On the subject of the transfer facilities, Mr Nair confirms that they were designed mainly by MAHB but with inputs from airlines. MAHB assumed in the design that about 50% passengers would be transfers though, interestingly, the airlines wanted an even higher percentage than that to be catered for.

Transfer facilities available within klia2 include domestic-to-domestic, domestic-to-international, international-to-domestic, and international-to-international. Transfers are applicable to both intra- and inter- airline services.

For the moment only about 10% of passengers are engaging in a transfer at klia2 but unlike its predecessor it was built very much with the future, and trends that are still evolving, in mind. By way of comparison, the percentage of transfer passengers at London Heathrow Airport, the world’s busiest international airport, was 37% in 2013, some way short of the MAHB target, let alone that of AirAsia and other airlines.

At London Stansted, which is referred to in this report, it is around 10% (but there is little or no airline encouragement for the activity there, indicating that a sufficiently wide network of routes alone may generate a certain level of connecting traffic). At Singapore Changi Airport, which has now dispensed with its LCT, the ratio was 30% in 2013.

It would appear that 50% is a tough target to achieve. If MAHB achieves it at klia2 it will indeed signal another sea change in the way airlines are managed where airports can help them facilitate such a change.

There are some known examples where airports have gone out of their way to facilitate self-connection between budget airlines, Cologne-Bonn airport in Germany, where self service transfer facilities were introduced, being a prime example. Further changes in airline operating procedures may demand that more airports rise to the challenge.

Parts of this report were paraphrased from the Low Cost Airports & Terminals Report, published by CAPA in 2009. The report is available for download at http://centreforaviation.com/reports/

Technical data sourced from the CAPA Airport Construction and Cap Ex database and from MAHB. For more information about subscriptions toCAPA's Airport Construction and Cap Ex database, contact info@centreforaviation.com

Source: Part 1, Part 2 – by centreforaviation.com

Site Search

Did you find what you are looking for? Try out the enhanced Google Search: